Insurance That Works as Hard as You Do

Public Liability Insurance in Jindabyne

Public liability insurance for Jindabyne businesses. Safeguard against costly third-party personal injury and property damage claims. Get covered today.

Understanding Your Cover – Jindabyne

Understanding Public Liability Insurance

Public liability cover shields your business across Jindabyne when a supplier, visitor, or member of the public experiences personal injury or property damage as a result of your business operations, whether on-site, at a client’s location, or anywhere your work takes you.

Without public liability insurance, your Jindabyne business could be personally liable for legal defence costs, compensation payouts, and associated expenses that run into the hundreds of thousands of dollars. Most industries also demand proof of cover before you can sign contracts or open your doors.

Public liability insurance in Jindabyne typically covers:

Without public liability cover for your Jindabyne business, your company may be personally liable for significant financial losses, putting everything you’ve built at risk.

$5M–$20M

Cover limits available

Multi-Insurer

Comparison access

Australia-Wide

Coverage provided

Policy Benefits

What’s Covered by Public Liability Insurance in Jindabyne?

Most public liability policies for Jindabyne businesses include:

Injury Liability Cover

If someone is injured as a result of your business activities, public liability insurance steps in to cover compensation and legal defence expenses for businesses in Jindabyne. Coverage extends to incidents both on and off your Jindabyne premises, wherever your work takes you

Property Damage Liability

If your work causes accidental damage to property belonging to a client, member of the public, or another third party, your public liability policy covers the cost of repair or replacement for your Jindabyne business. Without this cover, businesses in Jindabyne could face substantial out-of-pocket expenses for even a single accidental incident.

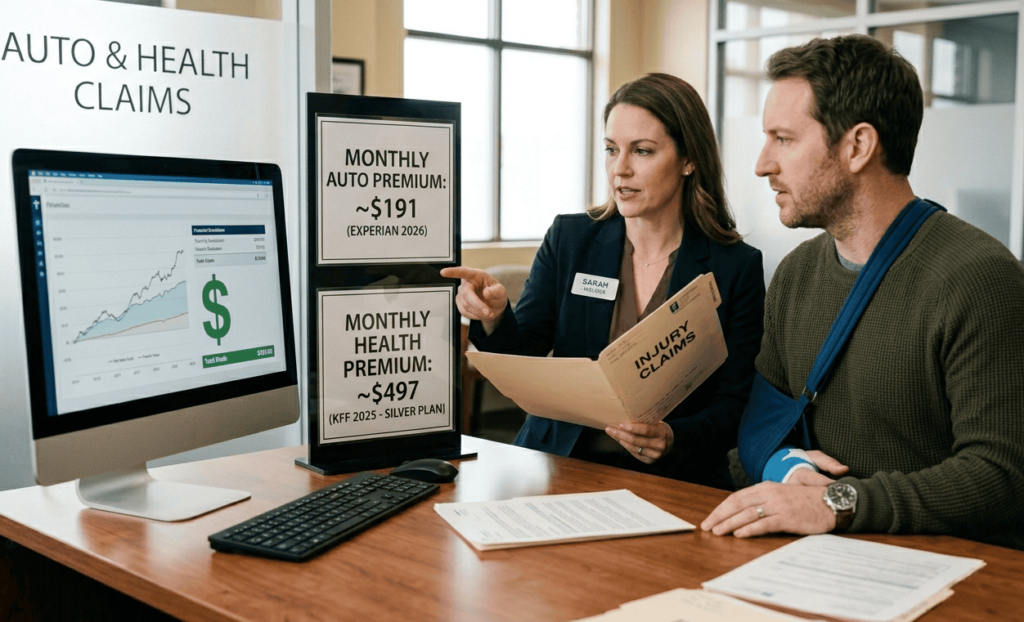

Legal Defence Costs

Defending a claim, even an unfounded one, can cost your Jindabyne business tens of thousands of dollars in legal fees alone. Businesses in Jindabyne are covered for solicitor fees, court costs, and related expenses, no matter how the claim is resolved. This ensures your Jindabyne business is never forced to settle a claim simply because you cannot afford to fight it.

Offsite and Mobile Business Cover

Your public liability policy travels with you beyond your Jindabyne business address, providing protection wherever your work takes you. Whether you’re working at a client’s home, a commercial site, a public venue, or any other location outside of Jindabyne, your policy covers incidents that occur in the course of your work. Speak with our team to confirm your offsite activities are fully covered under your Jindabyne policy.

Goods and Products Liability (Optional Extension)

Products liability cover is designed for businesses in Jindabyne that produce, wholesale, retail, or supply goods, covering claims where a product causes injury or property damage. This extension fills a critical gap for product based businesses in Jindabyne, ensuring that claims arising from defective, faulty, or harmful goods are covered. Our team works with businesses in Jindabyne to assess whether products liability cover should form part of your overall insurance solution.

Types of Cover

Choosing the Right Public Liability Cover in Jindabyne

Every business in Jindabyne carries a different level of risk. We’ll match your Jindabyne business with the right policy for your industry and activities.

General Public Liability Cover for Jindabyne Businesses

Broad third-party cover for injury and property damage suitable for most Jindabyne businesses, consultants, and service providers.

Product Liability Insurance in Jindabyne

Built for Jindabyne businesses that deal in physical products, covering injury or damage claims connected to goods sold through your Jindabyne business.

Trades Liability Insurance in Jindabyne

Built for tradies and contractors operating in and around Jindabyne.

Event Public Liability Insurance in Jindabyne

Protection tailored to events and functions held in Jindabyne. Arrange cover around your Jindabyne event schedule with flexible terms.

Is It Right for You?

Many contracts and licences in Australia require minimum cover amounts of $5M, $10M or $20M.

Who Needs Public Liability Insurance?

Why Jindabyne Businesses Choose Insurance Me Advisory

Public Liability Insurance Quotes for Jindabyne Businesses

Protect your Jindabyne business from unexpected claims and legal costs. Call us or fill out our contact form to get started.