Insurance That Works as Hard as You Do

Business Liability Cover for Taperoo

Public liability insurance for Taperoo businesses. Safeguard against costly third-party personal injury and property damage claims. Get covered today.

Understanding Your Cover – Taperoo

What is Public Liability Cover?

Public liability insurance shields your business throughout Taperoo when a supplier, visitor, or member of the public experiences property damage or bodily injury as a result of your day-to-day operations, whether at your premises, a worksite, or anywhere you operate.

Without public liability insurance, your business could be directly liable for legal defence costs, compensation payouts, and associated expenses that can easily reach six figures. Businesses across Taperoo also require proof of cover before you can legally trade or win contracts.

Public liability insurance in Taperoo typically covers:

Without public liability insurance in Taperoo, your business may be personally liable for substantial out-of-pocket costs, leaving your business financially vulnerable.

$5M–$20M

Cover limits available

Multi-Insurer

Comparison access

Australia-Wide

Coverage provided

Policy Benefits

What’s Covered by Public Liability Insurance in Taperoo?

Here’s what public liability insurance in Taperoo generally covers:

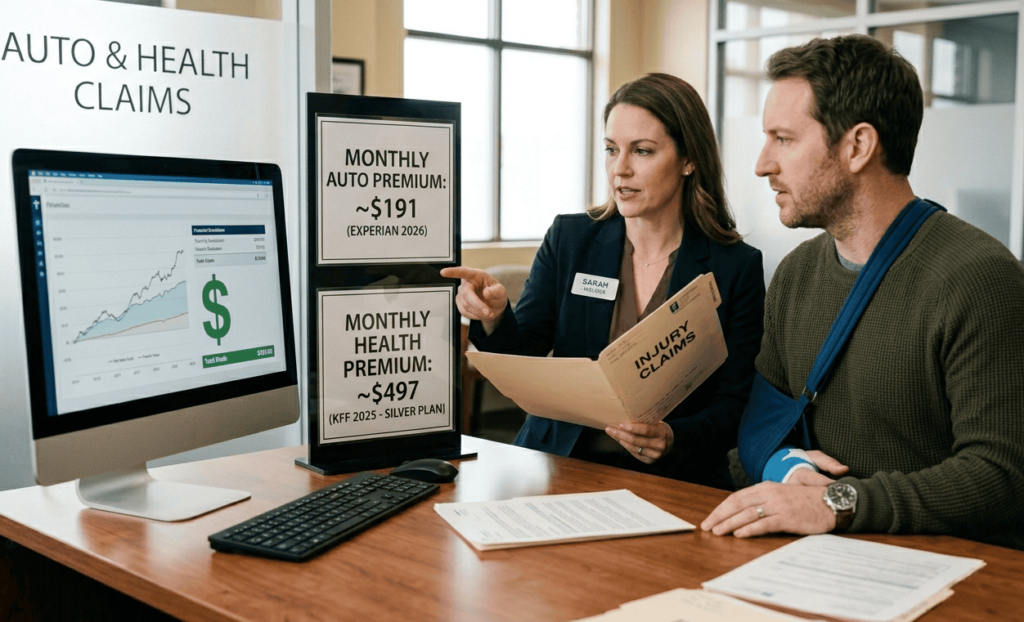

Injury Liability Cover

If someone is injured as a result of your business activities, your cover handles the financial burden of compensation and legal fees wherever your Taperoo business operates. Whether the injury happens at your Taperoo business premises or at an offsite location, you’re protected

Third-Party Property Damage

If your work causes accidental damage to property belonging to a client, member of the public, or another third party, your cover steps in to meet those costs so your Taperoo business is never left exposed. From minor incidents to significant property damage claims, businesses in Taperoo can operate with confidence knowing they’re protected.

Court and Legal Cost Cover

Defending a claim, even an unfounded one, can cost your Taperoo business tens of thousands of dollars in legal fees alone. Businesses in Taperoo are covered for solicitor fees, court costs, and related expenses, no matter how the claim is resolved. Having this cover means your Taperoo business can focus on the facts of the matter, not the financial pressure of mounting legal bills.

Offsite and Mobile Business Cover

Public liability insurance doesn’t just protect your Taperoo premises and cover extends to wherever your business operates. Whether you’re working at a client’s home, a commercial site, a public venue, or any other location outside of Taperoo, your policy covers incidents that occur in the course of your work. Always ensure your insurer is aware of all locations and activities your Taperoo business undertakes to avoid any gaps in cover.

Product Liability Cover (Optional Extension)

If your business in Taperoo deals in physical products at any stage of the supply chain, a products liability extension ensures you’re protected against claims arising from those goods. Without a products liability extension, businesses in Taperoo that deal in physical goods may be exposed to significant uninsured risk. Our team works with businesses in Taperoo to assess whether products liability cover should form part of your overall insurance solution.

Types of Cover

Types of Public Liability Insurance in Taperoo

Different Taperoo businesses have different risk profiles. We’ll match your Taperoo business with the right policy for your industry and activities.

Standard Public Liability Insurance in Taperoo

Core public liability protection designed for service-based businesses and professionals based in Taperoo.

Goods & Products Liability Insurance in Taperoo

Specifically designed for Taperoo businesses that manufacture, import, wholesale, or retail physical goods, essential cover for product-based businesses in Taperoo.

Trades Liability Insurance in Taperoo

Designed for tradies and contractors working on residential and commercial sites in Taperoo.

Event Liability Insurance in Taperoo

Flexible cover designed for Taperoo markets, festivals, trade shows, and corporate functions. Arrange cover around your Taperoo event schedule with flexible terms.

Is It Right for You?

Many contracts and licences in Australia require minimum cover amounts of $5M, $10M or $20M.

Who Needs Public Liability Insurance?

Why Taperoo Business Owners Trust Insurance Me Advisory

Get Your Taperoo Public Liability Quote Today

Don’t leave your Taperoo business exposed, get covered against unexpected claims and legal costs. Speak with one of our trusted advisers or complete our quick online form.